6 Consumption and credit constraints

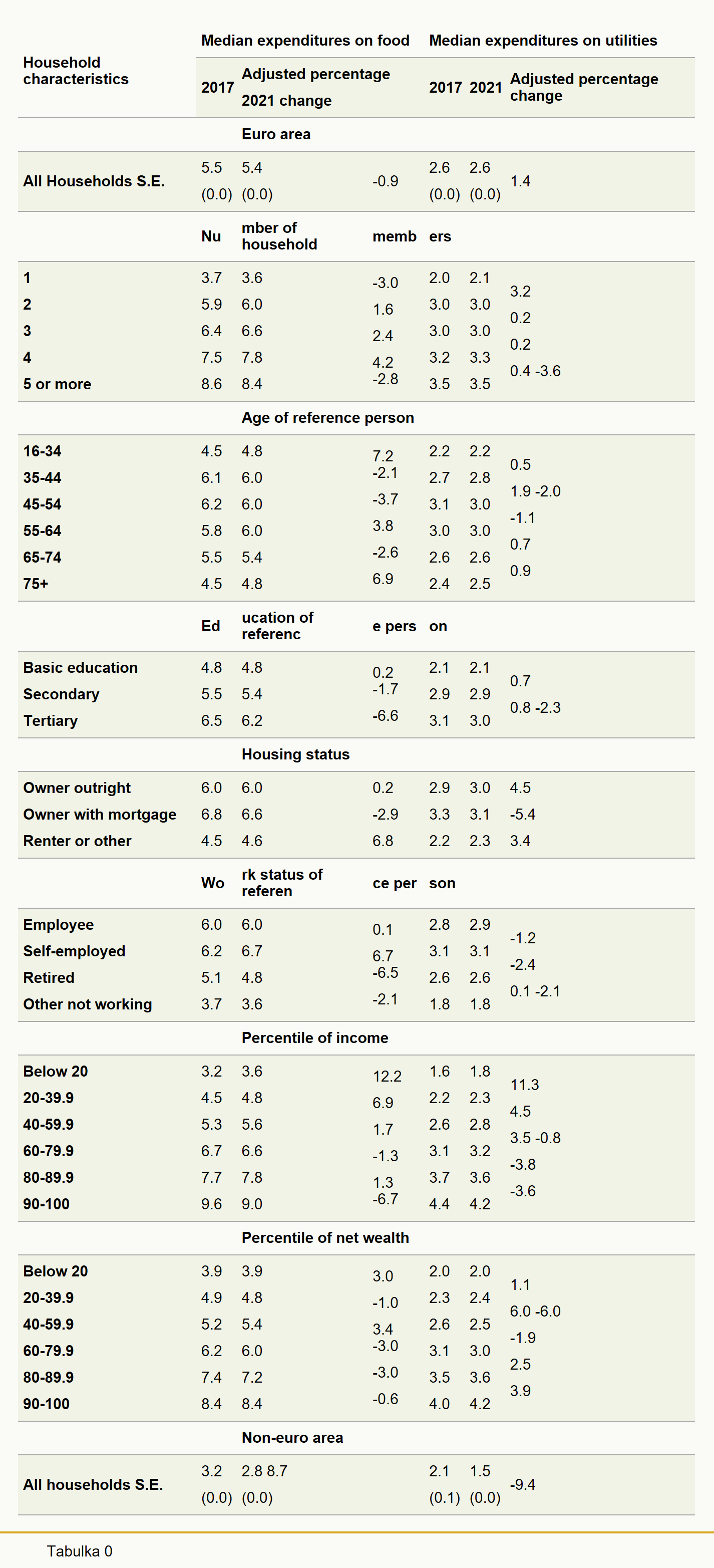

Between 2017 and 2021, the median annual value of food consumption remained roughly unchanged at around €5,500. The amount spent on utilities was also largely the same, at around €2,600 both in 2017 and 2021 (Table 11).

However, the changes become more pronounced across household groups. For example, median expenditures on food grew by around 7% for households below 35 years or age and those aged over 74 and tended to decline for middle aged households (ages 35-54). Spending on both food and utilities grew by at least 6.9% for the bottom two income quintiles, but did not increase much (or even decreased) in the top two quintiles. Similarly, the increase in spending was stronger in the lowest and the medium net wealth quintiles.

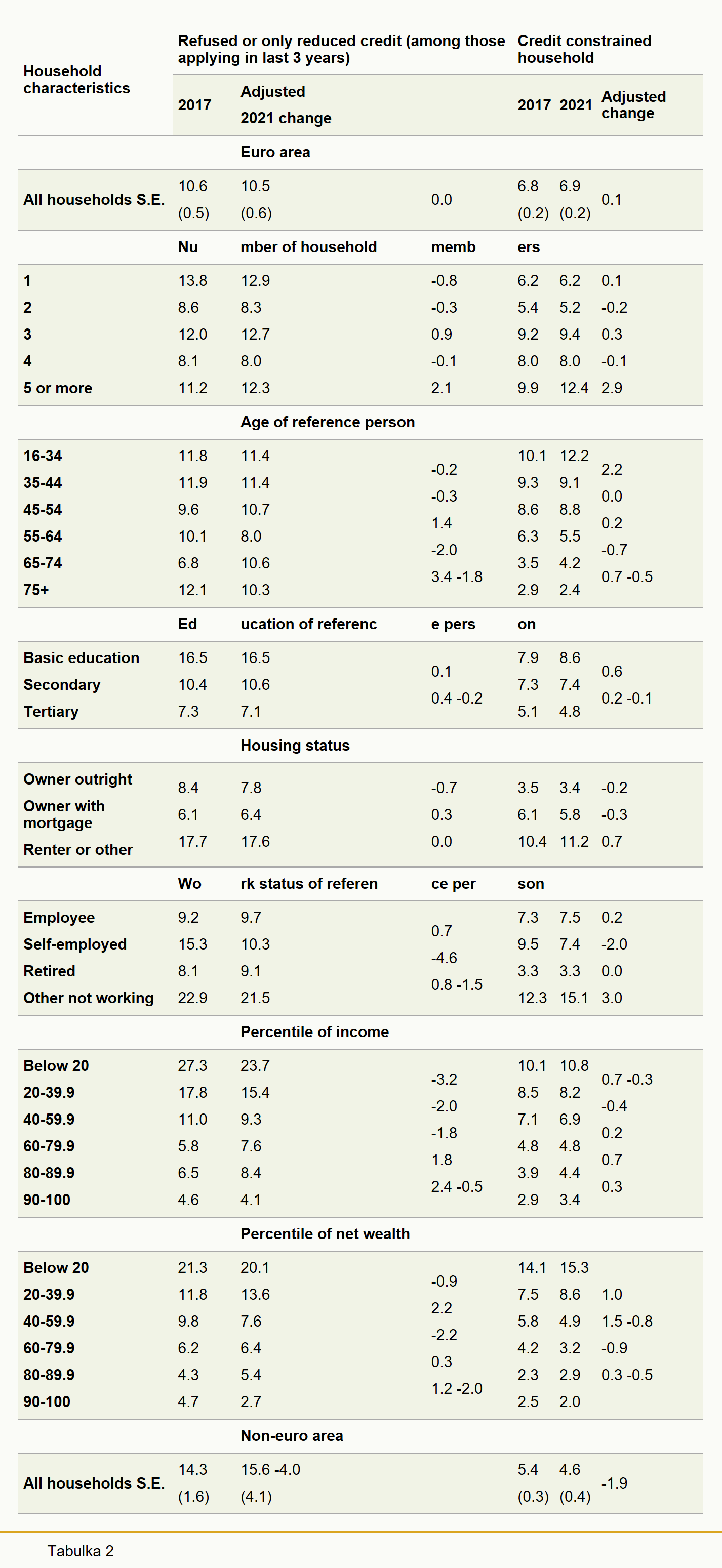

The share of households that had applied for credit within the last three years dropped slightly to 21.9% (Table 12A). The changes among all sub-groups of the population considered were relatively modest. The percentage of those that did not apply for credit because of perceived credit constraints increased marginally to 5.4%. Across the age distribution, the largest increases were seen among younger households, with the percentage climbing by 2.3 percentage points to 9.6% for those aged 16-34.

The proportion of households that were fully or partially refused a loan was broadly unchanged around 10.5% in 2021. A reduction across lower income quintiles was counterbalanced by increases in the upper part of the distribution.

These combined developments resulted in the proportion of credit-constrained households (as defined in the notes to Table 12B) increasing negligibly for most subgroups of the population, from 6.8% to 6.9% for the euro area as a whole.

11 Consumption

(thousands of 2021 EUR)

Household characteristics | Median expenditures on food | Median expenditures on utilities | ||||

2017 | Adjusted percentage 2021 change | 2017 | 2021 | Adjusted percentage change | ||

Euro area | ||||||

All Households S.E. | 5.5 (0.0) | 5.4 (0.0) | -0.9 | 2.6 (0.0) | 2.6 (0.0) | 1.4 |

Nu | mber of household | memb | ers | |||

1 2 3 4 5 or more | 3.7 5.9 6.4 7.5 8.6 | 3.6 6.0 6.6 7.8 8.4 | -3.0 1.6 2.4 4.2 -2.8 | 2.0 3.0 3.0 3.2 3.5 | 2.1 3.0 3.0 3.3 3.5 | 3.2 0.2 0.2 0.4 -3.6 |

Age of reference person | ||||||

16-34 35-44 45-54 55-64 65-74 75+ | 4.5 6.1 6.2 5.8 5.5 4.5 | 4.8 6.0 6.0 6.0 5.4 4.8 | 7.2 -2.1 -3.7 3.8 -2.6 6.9 | 2.2 2.7 3.1 3.0 2.6 2.4 | 2.2 2.8 3.0 3.0 2.6 2.5 | 0.5 1.9 -2.0 -1.1 0.7 0.9 |

Ed | ucation of referenc | e pers | on | |||

Basic education Secondary Tertiary | 4.8 5.5 6.5 | 4.8 5.4 6.2 | 0.2 -1.7 -6.6 | 2.1 2.9 3.1 | 2.1 2.9 3.0 | 0.7 0.8 -2.3 |

Housing status | ||||||

Owner outright Owner with mortgage Renter or other | 6.0 6.8 4.5 | 6.0 6.6 4.6 | 0.2 -2.9 6.8 | 2.9 3.3 2.2 | 3.0 3.1 2.3 | 4.5 -5.4 3.4 |

Wo | rk status of referen | ce per | son | |||

Employee Self-employed Retired Other not working | 6.0 6.2 5.1 3.7 | 6.0 6.7 4.8 3.6 | 0.1 6.7 -6.5 -2.1 | 2.8 3.1 2.6 1.8 | 2.9 3.1 2.6 1.8 | -1.2 -2.4 0.1 -2.1 |

Percentile of income | ||||||

Below 20 20-39.9 40-59.9 60-79.9 80-89.9 90-100 | 3.2 4.5 5.3 6.7 7.7 9.6 | 3.6 4.8 5.6 6.6 7.8 9.0 | 12.2 6.9 1.7 -1.3 1.3 -6.7 | 1.6 2.2 2.6 3.1 3.7 4.4 | 1.8 2.3 2.8 3.2 3.6 4.2 | 11.3 4.5 3.5 -0.8 -3.8 -3.6 |

Percentile of net wealth | ||||||

Below 20 20-39.9 40-59.9 60-79.9 80-89.9 90-100 | 3.9 4.9 5.2 6.2 7.4 8.4 | 3.9 4.8 5.4 6.0 7.2 8.4 | 3.0 -1.0 3.4 -3.0 -3.0 -0.6 | 2.0 2.3 2.6 3.1 3.5 4.0 | 2.0 2.4 2.5 3.0 3.6 4.2 | 1.1 6.0 -6.0 -1.9 2.5 3.9 |

Non-euro area | ||||||

All households S.E. | 3.2 (0.0) | 2.8 8.7 (0.0) | 2.1 (0.1) | 1.5 (0.0) | -9.4 | |

The table reports household consumption in 2017 and 2021.

There are two different indicators of household consumption, both referring to annual amounts: (1) total household expenditure on food, both at home and outside the home, and (2) total household expenditure on utilities. The first three sub-columns report the median annual food expenditure at home and outside the home in 2017 and in 2021, and the adjusted percentage change between those years, calculated using the historical weights for Italy. Sub-columns 4 to 6 show the median annual amount spent on utilities in those same years and the corresponding percentage change. All statistics are broken down by different household groups as follows: (1) all households, (2) number of household members, (3) age of the reference person, (4) education of the reference person, (5) housing status of the household, (6) work status of the reference person, (7) percentile of income within the euro area, (8) percentile of net wealth within the euro area and (9) all households in the non-euro area. Standard errors were calculated using the Rao-Wu rescaled bootstrap method and replicate weights provided by the countries (1,000 replicates). Adjusted percentage changes: for the euro area, percentage changes are computed with reference to an unchanged sample design and do not match the values that would be obtained by directly comparing the figures shown in the 2017 and 2021 columns; for the non-euro area aggregate, percentage changes are computed with reference to Hungary and Croatia only. Data are included for the following euro area countries in this table: Belgium, Germany, Estonia, Ireland, Greece, Spain, France, Italy, Cyprus, Latvia, Lithuania, Luxembourg, Malta, Netherlands, Austria, Portugal, Slovenia, Slovakia and Finland. Non-euro area comprise Croatia, Hungary and Poland in 2017; and Czech Republic, Croatia and Hungary in 2021. For the inflation adjustment of the 2021 wave, various HICP levels were used depending on the year in which the countries ran most of the fieldwork. More specifically, the HICP level in 2019 was used for Finland, the HICP level in 2020 was used for Ireland, Spain, Italy, Latvia, Malta and Portugal, and the HICP level in 2021 was used for all other countries.

12A

Credit constraints

(percentage of households)

Household characteristics | Applied for credit within last 3 years | Not applying for credit due to perceived credit constraint |

Adjusted 2017 2021 change | Adjusted 2017 2021 change | |

Euro area | ||

All households S.E. | 23.2 21.9 -1.5 5.2 5.4 0.2 (0.3) (0.3) (0.2) (0.2) | |

Number of household members | ||

1 2 3 4 5 or more | 14.7 13.0 -1.6 4.9 5.3 0.5 21.0 20.6 -0.5 4.0 4.0 0.0 32.7 30.3 -2.6 6.6 6.5 0.0 36.0 34.4 -2.3 6.2 6.2 -0.1 32.3 35.3 2.7 7.7 9.2 1.6 | |

Age of reference person | ||

16-34 35-44 45-54 55-64 65-74 75+ | 33.3 32.9 -0.7 7.3 9.6 2.3 34.4 33.3 -1.4 6.5 6.8 0.4 29.8 26.8 -3.3 6.9 7.0 0.1 21.7 21.3 -0.6 4.9 4.2 -0.6 12.8 12.6 -0.1 2.8 3.4 0.6 4.5 4.7 0.1 2.4 2.0 -0.4 | |

Education of reference person | ||

Basic education Secondary Tertiary | 15.8 16.0 0.2 6.2 6.9 0.5 24.6 22.8 -2.0 5.6 5.8 0.3 28.9 25.7 -3.3 3.6 3.6 0.2 | |

Housing status | ||

Owner outright Owner with mortgage Renter or other | 14.3 12.4 -1.9 2.7 2.7 0.0 47.9 45.3 -2.4 3.8 3.8 0.0 19.2 19.2 -0.3 8.4 9.2 0.6 | |

Work status of reference person | ||

Employee Self-employed Retired Other not working | 32.1 30.5 -2.3 5.2 5.4 0.2 30.1 25.1 -4.2 6.6 5.9 -0.5 10.1 9.6 -0.5 2.7 2.7 0.0 12.3 14.6 2.4 10.9 13.5 2.8 | |

Percentile of income | ||

Below 20 20-39.9 40-59.9 60-79.9 80-89.9 90-100 | 10.9 10.9 0.0 8.4 9.4 1.1 16.7 18.1 1.2 6.8 6.6 -0.2 23.1 23.2 -0.6 5.3 5.6 0.2 31.1 27.6 -3.6 3.4 3.2 0.1 33.5 28.2 -5.0 2.3 2.1 -0.1 35.0 30.8 -3.7 1.9 2.2 0.2 | |

Percentile of net wealth | ||

Below 20 20-39.9 40-59.9 60-79.9 80-89.9 90-100 | 21.5 21.9 0.2 11.6 13.0 1.2 22.6 23.0 -0.1 5.6 6.4 1.2 25.1 23.3 -2.2 4.0 3.6 -0.3 23.2 21.0 -2.2 3.2 2.1 -1.0 22.1 20.2 -1.5 1.6 2.0 0.1 24.9 20.2 -4.6 1.5 1.6 0.0 | |

Non-euro area | ||

All households S.E. | 11.7 76.5 63.4 4.8 4.2 -1.7 (0.4) (0.3) (0.3) (0.4) | |

The table reports credit constraints among households.

The first three sub-columns show the percentage of households that had applied for credit in the previous three years in 2017 and 2021, and the percentage point change from 2017 to 2021. Sub-columns 4 and 5 show those households that chose not to apply for credit owing to a perceived credit constraint and the percentage point change from 2017 to 2021. All statistics are broken down by different household groups, as follows: (1) all households, (2) number of household members, (3) age of the reference person, (4) education of the reference person, (5) housing status of the household, (6) work status of the reference person, (7) percentile of income within the euro area, (8) percentile of net wealth within the euro area and (9) all households in the non-euro area. Standard errors were calculated using the Rao-Wu rescaled bootstrap method and replicate weights provided by the countries (1,000 replicates). Adjusted percentage changes: for the euro area, percentage changes are computed with reference to an unchanged sample design and do not match the values that would be obtained by directly comparing the figures shown in the 2017 and 2021 columns; for the non-euro area aggregate, percentage point changes are computed with reference to Hungary and Croatia only. Data are included for the following euro area countries in this table: Belgium, Germany, Estonia, Ireland, Greece, France, Cyprus, Latvia, Lithuania, Luxembourg, Malta, Netherlands, Austria, Portugal, Slovenia, Slovakia and Finland. Non-euro area comprises Croatia, Hungary and Poland in 2017; and Czech Republic, Croatia and Hungary in 2021. For the inflation adjustment of the 2021 wave, various HICP levels were used, depending on the year in which the countries ran most of the fieldwork. More specifically, the HICP level in 2019 was used for Finland, the HICP level in 2020 was used for Ireland, Spain, Italy, Latvia, Malta and Portugal, and the HICP level in 2021 was used for all other countries.

12B

Credit constraints

(percentage of households)

Household characteristics | Refused or only reduced credit (among those applying in last 3 years) | Credit constrained household | ||||

2017 | Adjusted 2021 change | 2017 | 2021 | Adjusted change | ||

Euro area | ||||||

All households S.E. | 10.6 (0.5) | 10.5 (0.6) | 0.0 | 6.8 (0.2) | 6.9 (0.2) | 0.1 |

Nu | mber of household | memb | ers | |||

1 2 3 4 5 or more | 13.8 8.6 12.0 8.1 11.2 | 12.9 8.3 12.7 8.0 12.3 | -0.8 -0.3 0.9 -0.1 2.1 | 6.2 5.4 9.2 8.0 9.9 | 6.2 5.2 9.4 8.0 12.4 | 0.1 -0.2 0.3 -0.1 2.9 |

Age of reference person | ||||||

16-34 35-44 45-54 55-64 65-74 75+ | 11.8 11.9 9.6 10.1 6.8 12.1 | 11.4 11.4 10.7 8.0 10.6 10.3 | -0.2 -0.3 1.4 -2.0 3.4 -1.8 | 10.1 9.3 8.6 6.3 3.5 2.9 | 12.2 9.1 8.8 5.5 4.2 2.4 | 2.2 0.0 0.2 -0.7 0.7 -0.5 |

Ed | ucation of referenc | e pers | on | |||

Basic education Secondary Tertiary | 16.5 10.4 7.3 | 16.5 10.6 7.1 | 0.1 0.4 -0.2 | 7.9 7.3 5.1 | 8.6 7.4 4.8 | 0.6 0.2 -0.1 |

Housing status | ||||||

Owner outright Owner with mortgage Renter or other | 8.4 6.1 17.7 | 7.8 6.4 17.6 | -0.7 0.3 0.0 | 3.5 6.1 10.4 | 3.4 5.8 11.2 | -0.2 -0.3 0.7 |

Wo | rk status of referen | ce per | son | |||

Employee Self-employed Retired Other not working | 9.2 15.3 8.1 22.9 | 9.7 10.3 9.1 21.5 | 0.7 -4.6 0.8 -1.5 | 7.3 9.5 3.3 12.3 | 7.5 7.4 3.3 15.1 | 0.2 -2.0 0.0 3.0 |

Percentile of income | ||||||

Below 20 20-39.9 40-59.9 60-79.9 80-89.9 90-100 | 27.3 17.8 11.0 5.8 6.5 4.6 | 23.7 15.4 9.3 7.6 8.4 4.1 | -3.2 -2.0 -1.8 1.8 2.4 -0.5 | 10.1 8.5 7.1 4.8 3.9 2.9 | 10.8 8.2 6.9 4.8 4.4 3.4 | 0.7 -0.3 -0.4 0.2 0.7 0.3 |

Percentile of net wealth | ||||||

Below 20 20-39.9 40-59.9 60-79.9 80-89.9 90-100 | 21.3 11.8 9.8 6.2 4.3 4.7 | 20.1 13.6 7.6 6.4 5.4 2.7 | -0.9 2.2 -2.2 0.3 1.2 -2.0 | 14.1 7.5 5.8 4.2 2.3 2.5 | 15.3 8.6 4.9 3.2 2.9 2.0 | 1.0 1.5 -0.8 -0.9 0.3 -0.5 |

Non-euro area | ||||||

All households S.E. | 14.3 (1.6) | 15.6 -4.0 (4.1) | 5.4 (0.3) | 4.6 (0.4) | -1.9 | |

The table reports credit constraints among households.

The first three sub-columns show those that had applied for credit in the previous three years but were denied it or were offered a smaller amount than they had applied for, and the percentage point change from 2017 to 2021. Sub-columns 4 to 6 show the percentage of credit-constrained households in 2017 and in 2021, and the percentage point change from 2017 to 2021. A creditconstrained household is defined as a household to which one or more of the following situations apply: (i) applied for credit within the last three years but was turned down, and did not report a successful re-application, (ii) applied for credit but was not granted the full amount applied for, or (iii) did not apply for credit owing to a perceived credit constraint. Households with missing information on applying for credit or on not applying for credit due to a perceived credit constraint are not included. The information on credit constraints is not necessarily fully imputed for all countries; remaining missing values may cause slight numerical inconsistencies between the individual components and the composite credit-constrained household indicator. All statistics are broken down by different household groups, as follows: (1) all households, (2) number of household members, (3) age of the reference person, (4) education of the reference person, (5) housing status of the household, (6) work status of the reference person, (7) percentile of income within the euro area, (8) percentile of net wealth within the euro area and (9) all households in the non-euro area. Standard errors were calculated using the Rao-Wu rescaled bootstrap method and replicate weights provided by the countries (1,000 replicates). Adjusted percentage changes: for the euro area, percentage changes are computed with reference to an unchanged sample design and do not match the values that would be obtained by directly comparing the figures shown in the 2017 and 2021 columns; for the non-euro area aggregate, percentage point changes are computed with reference to Hungary and Croatia only. Data are included for the following euro area countries in this table: Belgium, Germany, Estonia, Ireland, Greece, France, Cyprus, Latvia, Lithuania, Luxembourg, Malta, Netherlands, Austria, Portugal, Slovenia, Slovakia and Finland. Non-euro area comprises Croatia, Hungary and Poland in 2017; and Czech Republic, Croatia and Hungary in 2021. For the inflation adjustment of the 2021 wave, various HICP levels were used, depending on the year in which the countries ran most of the fieldwork. More specifically, the HICP level in 2019 was used for Finland, the HICP level in 2020 was used for Ireland, Spain, Italy, Latvia, Malta and Portugal, and the HICP level in 2021 was used for all other countries.

Abbreviations

Countries

|

|

ISCO International Standard Classification of

Occupations

© European Central Bank, 2023

Postal address 60640 Frankfurt am Main, Germany

Telephone +49 69 1344 0

Website www.ecb.europa.eu

All rights reserved. Any reproduction, publication and reprint in the form of a different publication, whether printed or produced electronically, in whole or in part, is permitted only with the explicit written authorisation of the ECB or the authors.

This paper can be downloaded without charge from the ECB websiteor from RePEc: Research Papers in Economics. Information on all of the papers published in the ECB Statistics Paper Series can be found on the ECB’s website.

PDF ISBN 978-92-899-6180-6, ISSN 2314-9248, doi:10.2866/31818, QB-BF-23-005-EN-N

[1] When comparing evidence between the two waves, monetary values for the 2017 wave data are adjusted for inflation. Country-specific inflation rates, as measured by the Harmonised Index of Consumer Prices (HICP), are used for the adjustment and lead to an average increase in 2017-wave euro value data of approximately 5%. For the Czech Republic, Croatia and Hungary, results in local currency are converted into euro using the appropriate exchange rate.

[2] The reference person is loosely defined as the highest income earner in the household. See Chapter 2 of HFCN (2023), The Household Finance and Consumption Survey: Methodological report for the 2021 wave”, Statistics Paper Series, No. 45, European Central Bank, June.

[3] The first wave of the HFCS was conducted in 15 euro area countries; the second wave in 18 euro area countries, as well as in Hungary and Poland; the third wave in all 19 countries of the euro area in 2017, as well as in Croatia, Hungary and Poland; and the fourth wave in all 19 countries of the euro area in 2021, as well as the Czech Republic, Croatia and Hungary.

[4] See HFCN (2023), The Household Finance and Consumption Survey: Methodological report for the 2021 wave”, Statistics Paper Series, No. 45, European Central Bank, June.

[5] See HFCN (2023), op. cit.

[6] The values of assets, debt, income and consumption were adjusted for by multiplying the third-wave figures with the ratio between the yearly averages of the price level between the reference years in the third and fourth survey waves.

[7] For the Czech Republic, average over 2021; for Croatia, 2020; for Hungary, average from October 2019 to September 2020.

[8] See Survey on Italian Household Income and Wealth 2020” (2022), Banca d’Italia Statistics Series, 22 July.

[9] Further methodological updates, improving on accuracy and coverage, were made in France and Cyprus, where weights were revised across all waves, and in Ireland, where the dataset for wave 2017 was revised.

[10] The charts report results for available countries only. The list of questions on the impact of the COVID19 pandemic that were asked in various countries is given in the Appendix of HFCN (2023), The Household Finance and Consumption Survey: Methodological report for the 2021 wave”, ECB Statistics Paper No. 45, June 2023.

[11] While the results for Portugal were collected in a slightly different way and are not shown in the chart, they do support these findings. For example, in Portugal the percentage of households saving more than usual increased in 2020, as compared with 2017. The additional savings were mostly due to declines in expenditures, whereas in 2017 the increase in income was the predominant factor. The importance of unplanned savings increased when compared with 2017 and became the main reason for the increase in savings across all groups of households. Lastly, compared with 2017, there was a broadly based increase in the percentage of households investing their additional savings in deposits.

[12] To provide a measure of the statistical significance of the changes, standard errors caused by sampling and imputation of missing data are given for selected estimates. The findings highlighted in the report are significant or interesting in a broader context.

[13] . Self-employment business wealth is wealth obtained from a business run as sole proprietorship, as independent professional or in partnership, or from active participation in running limited liability companies.

[14] The reference year for income is 2019 for some countries and 2020 for others (Table 1 above). Income for the latter group was affected by fiscal measures aimed at protecting households from the adverse effects of the COVID-19 pandemic.

| Zařazeno | čt 20.07.2023 12:07:00 |

|---|---|

| Zdroj | ECB Publication |

| Originál | ecb.europa.eu//pub/pdf/scpsps/ecb.sps46~3563bc9f03.en.pdf |

RSS - všechny zprávy

RSS - všechny zprávy Vložit zprávy na www stránky

Vložit zprávy na www stránky

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}